15 Apr CIBC customers dinged when bank adds $5 fee to e-gift cards, calling them a ‘cash advance’

Catharine Murphy likes to send her friends and family e-gift cards — for special occasions, to mark a holiday, just say thank you, or to make up for missing a milestone.

“I’m the person who will always wish you a belated birthday,” she said with a laugh, during an interview at her home in Oakville, Ont.

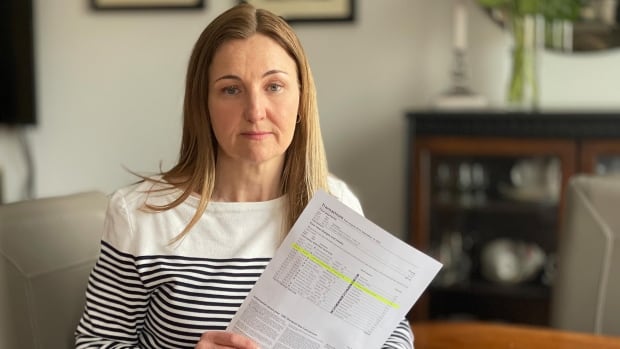

But last November as she reviewed her CIBC Visa credit card statement, Murphy noticed an additional $5 charge below a $10 Tim Hortons gift card she’d purchased for a son who is away at school.

She also saw another $5 charge for a second $10 Tim Hortons gift card Murphy had purchased for her daughter.

Curious, she dug out her October Visa statement and discovered the bank had also dinged her $5 when she bought a $25 Starbucks e-gift card for a friend that month. A gift card she purchased in August did not have the extra fee.

Murphy called CIBC to inquire about the extra charges and after a lengthy conversation with a customer service rep learned they were “cash advance” fees, charged every time anyone purchased a gift card that is sold by a company called CashStar.

That third party company sells gift cards online or via an app for more than 300 companies — many of them popular brands such as Tim Hortons, Starbucks, Best Buy, Home Depot, Lululemon and Sephora.

Murphy said it was “infuriating” to see a $5 cash advance fee on the purchase of a gift card — a fee that was accruing interest from the day of purchase at a rate of 22.99 per cent — not the usual 19.99 per cent charged on regular purchases only if the monthly credit card balance isn’t paid off.

On top of that, she says the CIBC rep couldn’t explain who was responsible for the charge — the bank itself, or CashStar.

Despite having her call escalated to a senior manager and calling back a few days later, Murphy says she couldn’t get any clarity about who was responsible for the charges.

Transparency important to customers

That lack of clarity is what consumers find most frustrating, especially when the big banks are making record profits, says a professor at the University of British Columbia’s Sauder School of Business.

“They should be upfront with what it is consumers are paying,” said Murali Chandrashekaran, who specializes in marketing and behavioural science. “It’s the transparency that’s more important than the actual pricing itself.”

When Go Public asked CashStar about the cash advance fee, a spokesperson said in a written statement that the company does not charge any additional fees, and that any cash advance fee would be “charged by the credit card issuer.”

CIBC declined an interview request, but in a statement a spokesperson said, “some gift cards purchased through third-party sellers are treated as cash-like transactions which can result in a cash advance fee.”

When Go Public asked the spokesperson for clarification, he said the fee was triggered by the transaction codes on some e-gift cards — but wouldn’t say why the charge suddenly kicked in last fall.

The bank said CIBC has now decided to scrap the fee, and will be automatically refunding cash advance charges for customers who used credit cards to purchase e-gift cards between Sept. 29, 2023 and Feb. 29, 2024.

The spokesperson declined to explain the reason for the bank’s about-face.

Angry customers question CIBC

Murphy has plenty of company on social media forums such as Reddit, where people with CIBC Visas, CIBC Mastercards and CIBC-owned Simplii credit cards have all noticed the $5 fee on their statements after purchasing e-gift cards.

Many reported that after waiting on the phone for up to an hour, a CIBC customer service rep agreed to refund the $5 fee as a one-time goodwill gesture.

That’s what a CIBC rep told Murphy, too, when she called her bank about the three $5 fees. The first agent she spoke to said she was only authorized to refund one of the extra fees.

“If I had been pressed for time on that day, I would have had to settle for that,” said Murphy. Instead, she escalated the call and got all three refunded.

Business professor Chandrashekaran says while a refund is nice, his research shows that what people want most is to be treated fairly, to hear a genuine apology from a company and a promise that it won’t happen again.

“The problem is that more often than not, companies will say, ‘OK, we’ll reverse this $5 dollars, but we’re going to do this just this once’ — as if they’re doing us a favour, and that demeans us,” he said.

“That lack of respect hurts the very foundation of trust.”

Despite people like Murphy and others complaining to CIBC about the fee as early as last September, the bank continued to charge the “cash advance” fee.

Possible Competition Act violations

Go Public reviewed CIBC’s Cardholder Agreement, which among other things, spells out what fees customers will be charged for various services when using their credit card. There was no mention of gift cards.

CIBC says a “cash advance” applies when using a credit card to withdraw money at a financial institution or ATM, making a bill payment with a credit card, or when transferring funds.

It says a “cash-like transaction” applies when using a credit card for a transaction “that is similar to cash” or buying an item that is “convertible into cash,” such as lottery tickets.

When asked why gift cards aren’t mentioned in the agreement, CIBC said it includes examples that are “illustrative” of what might prompt a cash advance fee.

As customers are not able to convert the e-gift cards in question into cash, the purchase should not be hit with a “cash advance” fee, said Chandrashekaran. What’s more, he says, adding an unexpected fee to a purchase may be a violation of the Competition Act.

University of British Columbia business prof Murali Chandrashekaran offers advice for CIBC customers who want to ensure they get the promised refund for $5 ‘cash advance’ fees on e-gift card purchases.

Two years ago, the federal government strengthened consumer protections in the Competition Act, to try to ensure the price Canadians see for a product is the one they pay.

“When a price is unattainable, because consumers must pay additional charges or fees to buy a product or service, it affects their abilities to make informed decisions,” reads an excerpt on the Competition Bureau’s website.

CIBC doesn’t sell the gift cards, said Chandrashekaran, but there is “zero transparency” about why they turn out to cost more than what the customer expected to pay.

“It’s up to consumers to decide whether they want to embrace this $5 or not,” he said. “Consumers were never given the opportunity to opt out of this situation.”

CIBC did not respond to Go Public’s request to comment on the fee being a possible violation of the Competition Act.

Bank fees cost Canadians billions: expert

The fee CIBC was charging is just the latest in a long list of bank fees Canadians dislike, said Chandrashekaran.

And now a report released in February by business consulting firm North Economics says Canadians pay “significantly higher” fees than many people in other countries.

The report estimates that Canadians could save $8.5 billion a year in bank fees — about $250 per adult — if banking regulators had a competition mandate, as exists in countries such as the U.K. and Australia.

CIBC was charging its credit card customers a $5 cash advance fee for e-gift card purchases until Go Public got involved.

“In Canada … no regulator is really paying attention to how competitive the banks are acting between each other,” said economist Alain de Bossard, managing director of North Economics, adding that the banks often seem to exhibit more co-ordinated than competitive behaviour.

“Certainly I think there are things that the government can do to improve the situation for Canadians,” said de Bossard.

Murphy says the experience has changed how she shops.

The last time she gave a friend a gift card, instead of buying one online, she drove to a store to purchase it and personally dropped it off.

“I have not sent an electronic gift card to anybody since I’ve had this run in,” said Murphy. “It was a blatant example of the bank taking advantage of people.”

Submit your story ideas

Go Public is an investigative news segment on CBC-TV, radio and the web.

We tell your stories, shed light on wrongdoing and hold the powers that be accountable.

If you have a story in the public interest, or if you’re an insider with information, contact gopublic@cbc.ca with your name, contact information and a brief summary. All emails are confidential until you decide to Go Public.